There are currently 97 mega-cap companies worldwide, each valued at $200 billion or more. To examine the companies shaping today’s markets, the team at BestBrokers analysed their industries, business models, and market valuations.

The concentration of market power among a small group of companies has become one of the defining features of modern financial markets – the so-called Magnificent Seven now account for roughly 35% of the S&P 500’s total value, up from just 12.5% a decade ago, a remarkable display of power among just seven companies.

At the same time, these firms are fueling an unprecedented wave of investment in artificial intelligence, pouring hundreds of billions of dollars into data centers, advanced chips, cloud infrastructure, and next-generation computing technologies, therefore, monitoring their growth, impact, and future direction has never been more important.

There are currently 97 mega-cap companies worldwide, each valued at $200 billion or more. To examine the companies shaping today’s markets, the team at BestBrokers analysed their industries, business models, and market valuations.

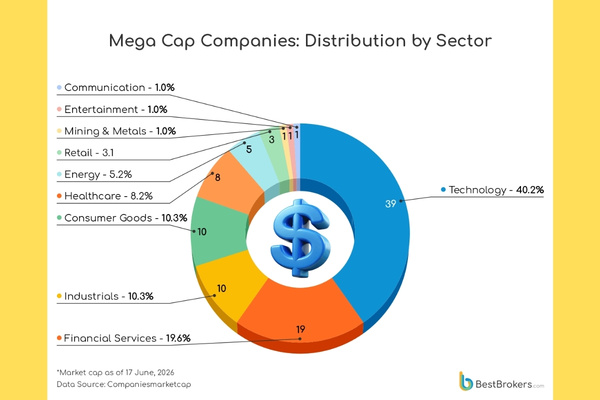

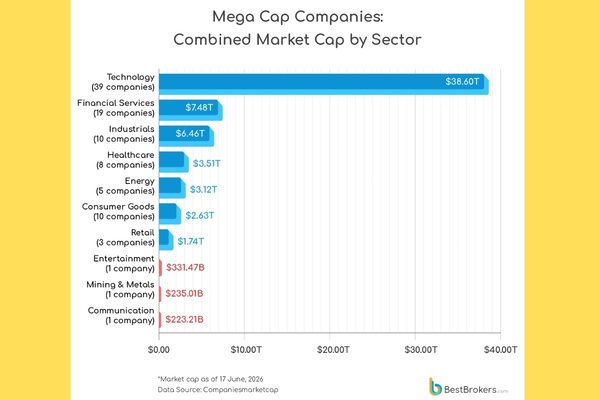

Although tech companies make up just 40% of the mega-cap universe, they account for roughly 60% of its total market value, with a combined capitalisation of $38.6 trillion.

This means that for every $10 invested across the world’s mega-cap companies, about $6 is tied to a technology firm.

The 10 largest mega-cap companies account for around 46% of total mega-cap market value, with a combined valuation of approximately $29.42 trillion. Eight of these top ten firms are technology-related, collectively representing nearly 39% of total mega-cap value, depicting how heavily global equity markets are now concentrated in the AI and digital infrastructure ecosystem.

At the very top of the rankings sit Nvidia, Alphabet, Apple, and Microsoft – four U.S. tech giants that together define much of the current market narrative, driven by leadership in artificial intelligence, cloud computing, digital advertising, and consumer ecosystems.

Their scale continues to set the tone for global equity performance, with movements in these names increasingly shaping broader index direction.

Outside the technology sector, SpaceX has emerged as one of the most closely watched newcomers on Wall Street following its record-breaking IPO in June 2026, which raised $75 billion and priced the company at around $1.7-1.8 trillion, making it one of the most valuable publicly traded firms in the world almost immediately after listing.

The stock has since seen intense volatility, briefly climbing into the top five global rankings before easing back, reflecting both strong retail investor demand and growing debate around its long-term valuation, particularly given its involvement with space infrastructure, satellite internet (Starlink), and emerging AI-linked projects such as space-based data systems.

The other non-tech entry is Saudi Aramco, the world’s largest oil producer, valued at roughly $1.8 trillion. Despite its scale, Aramco’s relative position in global rankings has gradually weakened in recent years.

At various points in 2022, it briefly competed for the title of the world’s most valuable company, even surpassing Apple during peak oil-price conditions. However, since then, its valuation has fallen from earlier highs above $2 trillion, reflecting softer oil prices, changing energy demand expectations, and a broader investor shift toward technology and AI-driven growth stocks.

Technology

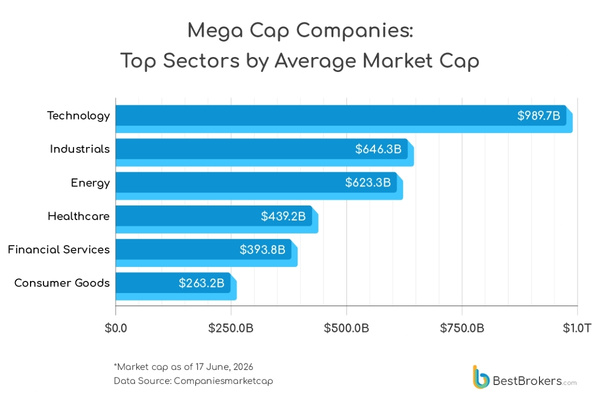

Technology is the dominant force in the mega-cap universe, with 39 companies among the 97, a combined market capitalisation of approximately $38.6 trillion, and an average market cap of around $989.7 billion – the highest across all sectors in every key metric.

This leadership is not only a matter of scale but also of concentration: a small group of AI- and semiconductor-driven/focused firms, including Nvidia, Apple, Microsoft, Alphabet, Amazon, TSMC, and Broadcom, account for a disproportionate share of total sector value and increasingly define global equity market direction.

The long-standing ‘FAANG’ grouping (Facebook/Meta, Apple, Amazon, Netflix, and Google/Alphabet), which once captured the dominance of consumer internet platforms, is increasingly being replaced by newer AI-focused classifications such as ‘MANGOS’.

The term is beginning to appear in ETF filings and market commentary to describe an emerging AI leadership narrative, and to show Wall Street’s fascination with the fruit aisle, referring to Meta, Alphabet/Google, Nvidia, and SpaceX, as well as AI companies Anthropic and OpenAI, although these two are yet to become public, making part of the fruit still not ripe enough.

This reflects a combination of publicly listed technology leaders and private AI developers, alongside related companies in areas such as computing and space infrastructure that are increasingly being viewed as part of the same broader AI-driven market trend.

Recent reporting also shows that asset managers have begun filing for ETFs linked to this theme, highlighting how AI-driven narratives are evolving from informal market labels into structured investment strategies.

Financial Services

The Financial Services category includes 19 companies with a combined market capitalisation of approximately $7.48 trillion, and an average market cap of around $393.8 billion.

The sector spans global banking giants, payment networks, investment firms, and diversified holding companies, with major representatives including JPMorgan Chase, Visa, Mastercard, Berkshire Hathaway, and leading Chinese state-owned banks.

What initially appears to be a structurally stable sector is increasingly defined by sharp divergence between traditional banking institutions and high-growth payment and investment platforms.

JPMorgan Chase has expanded aggressively into platform-based financial infrastructure, including its takeover of the Apple Card programme from Goldman Sachs, positioning itself deeper inside consumer payments ecosystems rather than traditional lending alone.

At the same time, Berkshire Hathaway has executed a notable portfolio reset under its new leadership structure, fully exiting long-held positions in Visa and Mastercard after more than a decade of ownership, signalling a shift away from payment networks even as transaction volumes remain structurally strong.

Meanwhile, payment companies are increasingly aligning themselves with the rise of AI-driven agents, where automated systems can initiate, route, and execute transactions on behalf of users, reinforcing their position at the centre of evolving digital commerce rather than being displaced by it.

This transition places networks like Visa and Mastercard within a broader re-rating of the payments landscape, as investors weigh traditional card rails against emerging fintech platforms, tokenised settlement systems, and next-generation AI-enabled payment flows.

Industrials

The Industrials category spans 10 companies with a combined market capitalisation of $6.46 trillion and an average value of approximately $646 billion per firm, the second-highest among the mega caps after tech giants.

The sector includes a mix of Aerospace (SpaceX, GE, RTX), Automotive (Tesla, Toyota), and industrial infrastructure companies such as Siemens and Caterpillar. Once viewed as a traditional economy sector, Industrials have become increasingly intertwined with some of today’s biggest investment themes.

The sector has been thrust into the spotlight in recent weeks by SpaceX’s record-breaking $75 billion IPO, the largest in history, which briefly pushed the company above a $2 trillion valuation and sparked renewed investor interest in the broader space economy. Meanwhile, companies linked to power generation, grid equipment, and electrification are benefiting from surging demand for the infrastructure needed to support the rapid expansion of AI data centres worldwide.

Consumer Goods

Consumer Goods also accounts for 10 companies with a total market capitalisation of $2.63 trillion and an average value of approximately $263 billion, making it one of the smaller mega-cap sectors by both scale and influence.

The sector is dominated by global brand leaders such as Procter & Gamble, Coca-Cola, Nestlé, LVMH, Hermès, Costco, and Zara parent Inditex.

Perhaps the most surprising development in Consumer Goods is that bigger brands are not necessarily winning.

Recent earnings have highlighted a growing split between companies built on scale and those built on scarcity, with luxury houses such as Hermès proving more resilient than many larger competitors, suggesting that brand exclusivity is still a valuable competitive advantage which appears to be outperforming ubiquity.

Healthcare

Healthcare comprises 8 mega-cap companies with a combined value of $3.51 trillion and an average market cap of approximately $439 billion, placing it firmly in the mid-to-upper tier of global sectors, with the sector anchored by pharmaceutical leaders such as Eli Lilly, Johnson & Johnson, Roche, Novartis, and AstraZeneca, alongside insurance and healthcare services groups like UnitedHealth.

Few sectors have undergone a more dramatic revaluation in recent years. The success of blockbuster weight-loss and diabetes therapies has created a new class of pharmaceutical giants, with Eli Lilly, the company behind Mounjaro, becoming one of the world’s most valuable companies and prompting investors to reassess the long-term growth potential of the healthcare and pharmaceuticals industry.

This rise of these next-generation obesity treatments has elevated pharmaceutical companies from defensive holdings into some of the market’s most closely watched growth stories, fundamentally changing investor perceptions of the industry’s future.

Energy

Energy is one of the most structurally underrepresented sectors, with only 5 companies and a combined valuation of $3.12 trillion, yet it stands out due to a relatively high average market cap of approximately $623 billion, driven primarily by Saudi Aramco.

The sector’s position highlights a notable market paradox: while investor attention has increasingly shifted toward AI and technology, oil and gas producers continue to rank among the world’s most valuable companies.

Recent geopolitical tensions in the Middle East have also renewed focus on energy security and supply risks, reminding markets that traditional energy remains a critical pillar of the global economy despite the rapid rise of digital industries.

Retail

Retail includes only 3 mega-cap companies, yet its influence far exceeds its size due to the scale and reach of Walmart, and Costco, and Home Depot with a combined market capitalisation of $1.74 trillion and an average value of roughly $579 billion per firm.

Walmart anchors mass retail and grocery consumption,

Costco leverages its membership-based wholesale model to drive high-volume value spending,

And Home Depot dominates U.S. home improvement demand tied to housing and renovation cycles.

Despite operating in different retail segments, all three benefit from strong brand loyalty, extensive physical networks, and significant pricing power, making this small group disproportionately important to the broader consumer economy.

Communication Services, Mining & Metals, and Entertainment

Each of these sectors has only one representative among the mega caps with a market capitalisation of over $200 billion – China Mobile (Communication Services), Netflix (Entertainment), and BHP (Mining & Metals). Each of these firms is effectively a ‘winner-takes-most’ outcome within structurally constrained industries.

China Mobile’s scale advantage is reinforced by its quasi-infrastructure role in China’s digital economy, where telecom operators are increasingly being repositioned as backbone providers of national AI and data infrastructure rather than purely consumer-facing carriers.

Netflix’s dominance reflects a different dynamic: Global distribution power combined with platform consolidation in streaming, where content libraries, recommendation systems, and now ad-supported monetisation layers are converging into a single scalable revenue engine.

Recent industry moves toward bundled streaming-podcast-live content ecosystems and ongoing M&A speculation around large media assets show how streaming leaders are transitioning from pure subscriber growth to multi-format attention platforms.

Meanwhile, BHP’s position is underpinned by its exposure to structurally tight commodity markets tied to electrification, AI infrastructure buildout, and energy transition supply chains, where demand for copper, iron ore, and related inputs remains resilient even as pricing cycles fluctuate.

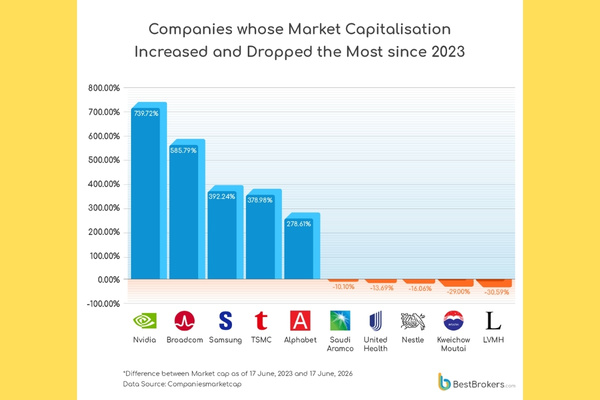

Nvidia, Broadcom & Samsung: The Boom of AI and Datacenters Driving Massive Expansion

When looking at the past three years, NVIDIA broke all existing records when it comes to growth, with its market capitalisation surging over 739% since 2023, driven primarily by its dominant position in AI computing infrastructure and accelerating demand for advanced GPUs powering large-scale data centres and generative AI models.

Chipmaker Broadcom ranks second with growth of almost 586%, which propelled it into the top tier of global mega-caps and the 8th largest company by market value, supported by strong exposure to AI networking chips, custom silicon, and enterprise connectivity demand that surged alongside hyperscaler infrastructure expansion.

Samsung, TSMC, and Alphabet round out the top five, all benefiting from their central roles in the AI supply chain, from advanced chip manufacturing to cloud platforms and digital advertising ecosystems, with semiconductor capacity constraints and AI-driven capex cycles acting as key tailwinds across the period.

As mentioned above, Saudi Aramco has been in steady decline over the period, reflecting softer oil prices, shifting global energy expectations, and a gradual rotation of capital toward technology and growth equities.

Health insurance provider UnitedHealth, Swiss food and beverage leader Nestlé, and Kweichow Moutai, China’s leading premium baijiu producer, renowned for its luxury brand, pricing power, and exceptional profitability, have all recorded negative growth, as healthcare, consumer staples, and reliance on China-linked consumer spending have faced margin pressure, slower growth expectations, and weaker investor sentiment amid macroeconomic uncertainty and changing consumption patterns.

The steepest decline is observed in the market capitalisation of LVMH, the massive French conglomerate owning brands such as Christian Dior, Louis Vuitton, Givenchy, and Kenzo among others.

The company’s market value has fallen by roughly 30% over the period, as the luxury sector normalises after post-pandemic demand surges, with weaker Chinese discretionary spending and a broader slowdown in high-end consumption weighing on revenue growth and valuation multiples.

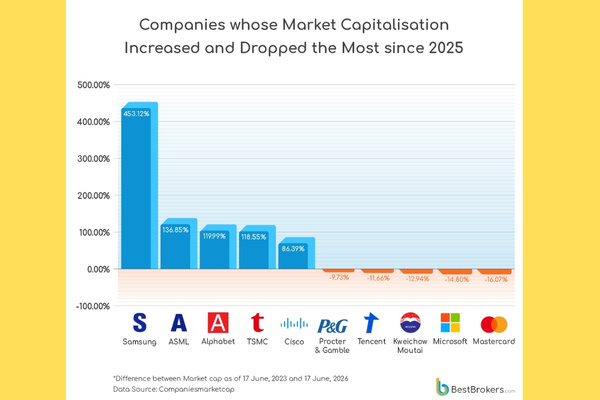

When looking at the more short-term performance, over a 1-year period, however, a notable reshuffling is seen in the leadership of mega-cap companies.

Nvidia is no longer present in the top cohort, giving the crown to Samsung, which surged 453% year-over-year, driven by rising demand for high-bandwidth memory (HBM) and other advanced DRAM products used in AI data centres, as well as a broader increase in memory pricing.

Dutch supplier to the semiconductor industry ASML follows with a market cap growth of 137% due to unprecedented demand for its Extreme Ultraviolet (EUV) lithography machines, which are critical for manufacturing advanced AI chips.

Another key new entrant is networking equipment provider Cisco, which returned to prominence with 86% growth, driven by renewed enterprise networking demand and infrastructure upgrades associated with AI data centre expansion.

Leading the 1-year declines, again, a very different set of names appears, highlighting a shift away from pandemic-era defensives and prior cycle leaders.

Procter & Gamble (-9.7%), the company behind household and personal care brands such as Gillette, Oral-B and Pantene, reflects cooling pricing power in consumer staples as input costs stabilise and demand normalises across developed markets, while Tencent (-11.7%), the Chinese technology giant whose businesses span social media, gaming, digital payments, cloud services, and online advertising, and Kweichow Moutai (-12.9%) continue to face regulatory pressure, weaker domestic consumption trends, and a broader slowdown in Chinese discretionary spending.

Microsoft (-14.8%) marks a notable pullback after years of AI-driven rerating, as investors rotate selectively within the technology sector rather than rewarding all large-cap software companies uniformly.

Mastercard (-16.1%) similarly reflects a cooling in payments-sector sentiment, with markets increasingly pricing in competition risks from fintech platforms and alternative payment rails despite structurally strong transaction volumes.

Methodology

This analysis is based on the full universe of mega-cap companies (market capitalisation of $200 billion or more), compiled using data from CompaniesMarketCap.com as of 17 June 2026.

The dataset includes 97 publicly listed firms across global equity markets. Each firm was classified by country, sector, and industry, and figures were aggregated to calculate total and average market capitalisation by sector, enabling cross-sector comparison of size, concentration, and market dominance.

We supplemented this with 3-year (2023-2026) and 1-year (2025-2026) shifts in the market capitalisations to distinguish between long-term structural winners and more recent cyclical shifts in performance, particularly those driven by artificial intelligence, semiconductor cycles, and evolving macroeconomic conditions.

{kind=link}