AI servers are now the main engine behind a sharp spike in high-end MLCC demand, and the market is starting to show the kind of tension that precedes a genuine supply constraints.

AI servers ignite high-end MLCC demand

TrendForce’s latest research shows rapid AI server upgrades and a ramp-up in custom ASICs from major cloud players are driving strong demand for high-capacitance, low-voltage, miniature MLCCs.

Platforms like Google TPU, AWS Trainium and Meta MTIA are packing more MLCCs onto accelerator boards, displacing traditional capacitor types and pushing per-board counts higher.

As a result, MLCCs used in AI infrastructure have become one of the fastest-growing passive component segments in both volume and value, with AI-led demand now clearly outpacing the sluggish consumer electronics side of the market.

Book-To-Bill ratios at Post-Pandemic Highs

By late June 2026, book-to-bill ratios at key Japanese and Korean suppliers like Murata, Samsung Electro-Mechanics (SEMCO) and Taiyo Yuden had climbed to 1.30, 1.31 and 1.25, the highest levels seen since the COVID-19 era.

The broader MLCC industry has also moved into positive territory, with the overall book-to-bill ratio reaching 1.04 and signalling solid order momentum across the supply chain.

Murata’s first-quarter 2026 numbers are especially telling, its orders-to-backlog ratio hit 1.27, surpassing the peak recorded during the severe MLCC shortage in 2018 and pointing to backlogs building faster than capacity can comfortably absorb.

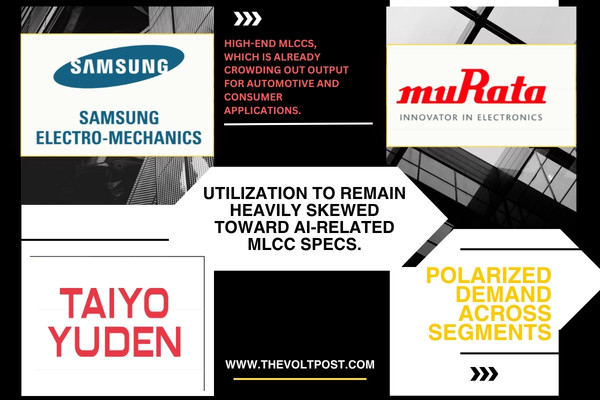

Polarized demand across segments

Demand is now clearly split between AI infrastructure and traditional consumer electronics. In the US, elevated inflation and high interest rates are eroding consumer spending power, weighing on smartphones and notebooks and keeping mainstream MLCC demand muted.

At the same time, Intel and AMD have shifted CPU production toward AI workloads, tightening supply for conventional PCs and forcing ODMs into urgent spot buys that raise component costs.

In contrast, high-capacitance, low-voltage, miniaturized MLCCs continue to see strong traction as cloud providers roll out custom AI accelerators and rework boards to accommodate more MLCCs per system.

Supply-side crowding and early buying

On the supply side, capacity is being pulled toward AI-focused, high-end MLCCs, which is already crowding out output for automotive and consumer applications.

Apple’s supply chain has started building inventory one to two months earlier than usual, while automotive ODMs have moved procurement forward from July to May, signalling real concern about availability in the second half of 2026.

In China’s Huaqiangbei and other distribution hubs, prices for mainstream X5R consumer-grade MLCCs have begun to climb, with typical increases in the 15 to 25 percent range.

As Japanese and Korean manufacturers prioritize higher-margin AI orders, spillover demand for mid- to high-capacitance X5R parts is expected to benefit Taiwanese and Chinese suppliers such as Yageo, Walsin Technology and Viiyong in the third quarter.

Second-half 2026 outlook and shortage risk

Looking ahead to the second half of 2026, TrendForce expects capacity utilization to remain heavily skewed toward AI-related MLCC specs as new accelerator platforms from NVIDIA, Google and AMD move into mass production in the third quarter.

Combined with customers’ early inventory-building, that tilt is likely to lengthen lead times and support further price increases for high-end MLCCs through year-end.

Combined with customers’ early inventory-building, that tilt is likely to lengthen lead times and support further price increases for high-end MLCCs through year-end.

The fourth quarter of 2026 emerges as the key inflection point where it will reveal whether the market tips from tightness into a full-blown shortage in high-end MLCC.

To Know More About TrendForce’s Semiconductor Reports And Market Data, CLICK HERE

{kind=link}