The semiconductor supply chains are an intricate global web of high-tech processes that transform raw materials into the world’s most advanced computing chips. It is not linear, but modular and interdependent, often spanning over 70 international touchpoints from design to delivery. Each node in the chain is highly specialized, making substitutions nearly impossible in the short term.

Original image created by The Volt Post Design Team. Base map elements from ©OpenStreetMap contributors. Icons under Flaticon CC license.

The semiconductor industry is the nerve centre of the global digital economy. From enabling autonomous vehicles and 5G networks to powering artificial intelligence and advanced defense systems, semiconductors are ubiquitous.

Yet, this trillion-dollar sector stands on an incredibly fragile supply chain that has been severely stress-tested over the past few years. The recent disruptions have exposed systemic vulnerabilities, reshaping how the world views semiconductor manufacturing, trade, and resilience.

The Strategic Importance of Semiconductor Supply Chains

The semiconductor supply chains are an intricate global web of high-tech processes that transform raw materials into the world’s most advanced computing chips.

It is not linear, but modular and interdependent, often spanning over 70 international touchpoints from design to delivery. Each node in the chain is highly specialized, making substitutions nearly impossible in the short term.

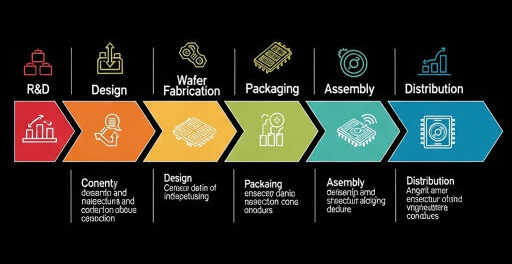

Illustration by The Volt Post. Value chain data from SIA and Deloitte Semiconductor Reports.

Breakdown of the Semiconductor Value Chain:

-

Design/IP (U.S., U.K., Israel): Companies like NVIDIA, AMD, and Arm design chips but rely on others for production.

-

Fabrication (Taiwan, South Korea, U.S.): Foundries like TSMC, Samsung, and Intel handle the actual production using nanometer-scale lithography.

-

Equipment (Netherlands, Japan, U.S.): ASML (EUV), Tokyo Electron, and Applied Materials supply the ultra-complex machines.

-

Materials (China, Japan, Germany): From photoresists to ultrapure gases and silicon wafers.

-

Packaging & Testing (Malaysia, Philippines, Vietnam): Backend processes that enable final assembly and quality control.

Any delay or restriction in even one of these phases can paralyze the entire downstream industry, including consumer electronics, aerospace, and critical infrastructure.

Current Challenges Facing the Semiconductor Supply Chains

1. Geopolitical Risks and Protectionism

The U.S.-China tech rivalry has led to export controls, blacklists, and supply embargoes. The U.S. has restricted access to cutting-edge chips and tools for Chinese firms like SMIC and Huawei.

In retaliation, China has limited exports of rare earth elements and chipmaking materials like gallium and germanium.

Data compiled from ASML, Tokyo Electron, and McKinsey reports. Graphic design by The Volt Post.

This tit-for-tat has created a bifurcated tech ecosystem, where parallel supply chains are emerging based on geopolitical allegiances. Such fragmentation reduces efficiency and increases duplication of infrastructure.

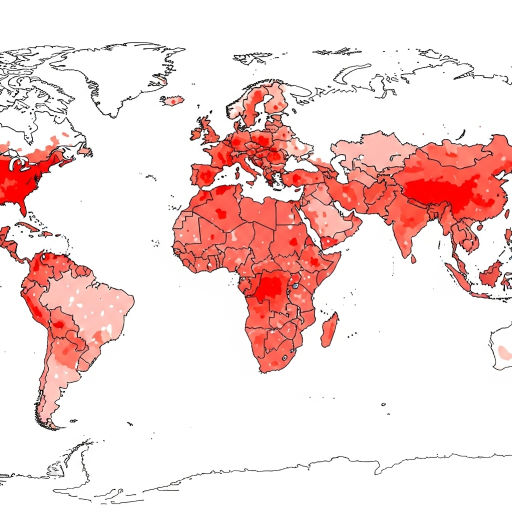

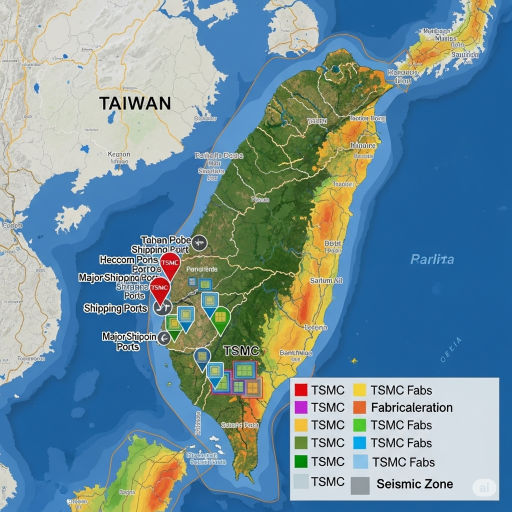

2. Concentration Risk

Over 90% of the world’s most advanced logic chips (below 10nm) are manufactured by TSMC in Taiwan. The island sits on the Pacific Ring of Fire, prone to earthquakes and typhoons, and is at the center of military tensions with China.

Data from SEMI 2025 Workforce Report. Heatmap created by The Volt Post.

Similarly, Samsung in South Korea dominates memory chip production. This geographical clustering exposes the industry to single points of failure—a strategic concern for national security, especially in defense and critical infrastructure sectors.

3. Supply-Demand Mismatch

The pandemic created a “bullwhip effect” where demand projections became erratic:

-

Consumer electronics surged during lockdowns.

-

Automotive chip orders were slashed, but quickly rebounded, creating shortages.

-

Legacy nodes (28nm and above), critical for cars and industrial IoT, were deprioritized by foundries chasing higher-margin 7nm/5nm orders.

This mismatch revealed the lack of agility and low transparency in demand forecasting, especially across Tier 2 and Tier 3 suppliers.

4. Equipment and Materials Shortages

Chip fabrication tools, especially ASML’s EUV lithography machines, are not just expensive (~$150 million per unit) but also slow to produce. Long lead times (up to 18 months) and export restrictions further constrain global capacity.

Additionally, raw material refining (e.g., high-purity polysilicon, copper foils, and sputtering targets) is limited to a few suppliers, many of which are located in politically unstable or resource-scarce regions.

5. Skilled Talent Deficit

Semiconductor manufacturing requires a specialized, high-skilled workforce in electrical engineering, cleanroom operations, quantum physics, and AI-driven process control. As older engineers retire, the talent pipeline has not kept pace, especially in countries trying to onshore chip production.

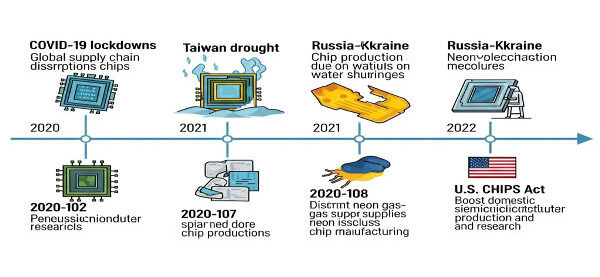

Impact of Supply Chain Disruptions

Original visual created by The Volt Post editorial team. Event data sources: Bloomberg, Reuters, Semiconductor Industry Association.

A. Industrial Impact

-

Automotive Sector: Automakers lost over $210 billion in revenue between 2021–2023 due to chip shortages, affecting production of over 13 million vehicles globally.

-

Consumer Electronics: Smartphone makers delayed launches and reduced feature sets due to lack of specific microcontrollers or sensors.

-

AI Acceleration Slowed: Limited access to high-performance GPUs and FPGAs impacted AI training and inferencing capabilities in cloud data centers.

Taiwan’s strategic centrality to chipmaking is also its greatest risk—TSMC fabs sit near active fault lines.

Base map © Google Maps (for illustrative editorial use). Data overlay created by The Volt Post using USGS seismic data.

B. Macroeconomic Impact

-

Inflationary Pressures: Semiconductor shortages cascaded into higher prices across consumer goods, contributing to post-COVID inflation.

-

GDP Drag: Countries like Germany, heavily reliant on high-end manufacturing and automotive exports, saw lowered GDP projections due to chip unavailability.

C. National Security Risks

Chips are essential for missile guidance, radar systems, drones, and satellites. Countries dependent on foreign semiconductor technology are exposed to critical risks in times of conflict or trade disputes.

How Can the Supply Chain Be Streamlined?

1. End-to-End Supply Chain Visibility

Use Digital Twins, blockchain, and AI to map and simulate the supply chain in real-time. Proactive risk management and predictive analytics can flag disruptions before they escalate.

Custom illustration by The Volt Post. World map base ©OpenStreetMap contributors, modified under ODbL.

2. Modular Capacity Expansion

Encourage “plug-and-play” fabrication modules that can be activated regionally in times of crisis. Think of flexible fabs, co-located with regional demand clusters.

3. Decentralized Sourcing

Shift from single-supplier models to diversified Tier 1, 2, and 3 vendors across different geographies. Use dual-sourcing strategies for critical components like substrate laminates and lithographic masks.

4. Precompetitive Collaboration

Competitors should collaborate on R&D for infrastructure, materials, and environmental controls. Industry alliances such as SEMI and RISC-V International can play a major role in standardization and knowledge sharing.

Top Countries for Semiconductor Supply Chains Diversification

Image © ASML Holding NV (press media kit – used under editorial license).

| Country | Advantages | Key Developments |

|---|---|---|

| United States | Advanced R&D, equipment leadership | CHIPS and Science Act ($52B), Intel and TSMC fabs in Arizona |

| India | Talent surplus, policy momentum | $10B India Semiconductor Mission; Micron OSAT plant in Gujarat |

| Germany | EU integration, auto-grade chip expertise | Intel €30B fab in Magdeburg, Infineon fab expansion |

| Japan | Precision equipment, materials | R&D alliance with U.S.; Rapidus building 2nm fab |

| Singapore | Logistics, IP laws | Micron, GlobalFoundries expanding DRAM and foundry capacity |

| Malaysia | OSAT and backend strength | AT&S, Infineon, and ASE investing in advanced packaging |

| Vietnam | Assembly and electronics ecosystem | Rising as an Apple and Samsung assembly alternative |

How Can the Supply Chain Disruption Problem Be Addressed?

1. Policy Interventions

Governments must offer long-term incentives, not just CapEx subsidies, but also tax credits, green energy, and fast-track land approvals. Establish strategic chip reserves, akin to oil reserves, for national emergencies.

2. Workforce Revamp

-

Fund universities and vocational institutes to produce next-gen chip designers, materials scientists, and cleanroom specialists.

-

Attract foreign talent with streamlined immigration policies.

3. Sustainability and ESG Integration

Fabrication plants consume massive amounts of water and power. Future fabs must integrate net-zero carbon targets, closed-loop water systems, and local community engagement to be viable.

4. Cyber-Resilience

Protect the semiconductor supply chain from cyber-espionage, IP theft, and ransomware attacks by hardening digital infrastructure across the lifecycle.

Conclusion: Toward a Resilient Semiconductor Ecosystem

The global semiconductor industry is not just a business sector—it is a strategic lifeline for national security, economic competitiveness, and innovation leadership. Strengthening its supply chain means:

-

Diversifying geography while maintaining quality.

-

Building trust-based alliances for cross-border cooperation.

-

Empowering next-gen talent to operate increasingly complex facilities.

In the face of growing uncertainties, the path forward lies in a coordinated global effort to build a resilient, transparent, and future-ready Semiconductor Supply Chains that powers progress for decades to come.

{kind=link}